About

Services

Industries

Press & insights

resources

contact

BLS & Co. periodically revises the state incentive pages to ensure our firm is providing the most current information on legislative and regulatory developments affecting available programs. Updates will be posted in the near future. In the interim, please call BLS & Co. with any questions at 609.924.9775 or reach out via email at info@BLSstrategies.com.

Discretionary Grant Funds: South Carolina offers three discretionary grant funds administered by the Coordinating Council for Economic Development: the Economic Development Set-Aside Program, the Closing Fund, and the Rural Infrastructure Fund. These grants are awarded on a case-by-case basis to support costs such as site preparation, road, water, sewer, and infrastructure improvements. The Set-Aside Program facilitates business development through infrastructure upgrades, while the Closing Fund provides additional funding for high-impact projects involving real property and infrastructure improvements. The Rural Infrastructure Fund targets Tier III and Tier IV counties, focusing on job creation and product development in rural areas.

Job Development Credit: This discretionary program offers a quarterly cash refund, calculated as a portion of the personal income tax withholdings of new employees. To qualify, businesses must meet industry requirements as defined by the program, create at least 10 full-time jobs within the project agreement period, provide wages at or above the county average, and offer a comprehensive benefits package covering at least 50% of the cost of employee health plan premiums. For service facilities, additional thresholds may apply regarding job creation and wage levels. The amount of the refund is influenced by factors such as the tier designation of the county where the project is located and the wages of the new employees. The grant is capped at $3,250 per employee per year. Businesses may claim the credit for up to 10 years, contingent on maintaining the job creation and investment commitments specified in their Revitalization Agreement. Refunds are restricted to reimbursing eligible capital expenditures, such as land, buildings, site improvements, or infrastructure, and cannot be used to offset state tax liabilities.

Jobs Tax Credit: Businesses that create a monthly average of at least 10 net new jobs at a corporate headquarters, manufacturing, distribution, processing, warehousing, agribusiness, or R&D facility can earn a credit equal to $1,500 to $25,000 per job annually, based on the county’s tier. Qualified service facilities may qualify if they meet stricter thresholds in Tier I–III counties (25–175 new jobs, depending on wage multipliers or building vacancy) or create 10 jobs in Tier IV counties. Small businesses with fewer than 99 employees qualify with just 2 net new jobs, but reduced credits apply for jobs paying under 120% of the county’s average wage. The credit can be applied against corporate income tax or premium tax and is non-refundable and capped at 50% of tax liability per year. Companies in multi-county industrial parks earn an additional $1,000 per job. The credit is available for five years, starting in year 2, and unused credits may be carried forward up to 15 years.

Corporate Headquarters Tax Credit: Companies establishing or expanding a corporate headquarters facility in South Carolina may receive a tax credit equal to 20% of qualifying real property costs associated with the portion of the facility dedicated to headquarter functions, or the first five years of direct lease costs. The credit can be applied against corporate income tax or license fees. To qualify, businesses must create at least 40 full-time jobs with wages at least twice the state per capita income. The facility must serve as the sole corporate headquarters for the region and handle the majority of corporate staff functions. The credit is non-refundable and can be carried forward for up to 10years. Credits are transferable to a succeeding taxpayer if the headquarters assets are sold. R&D activities directly tied to headquarters operations are also eligible for the credit, expanding its applicability beyond traditional corporate functions.

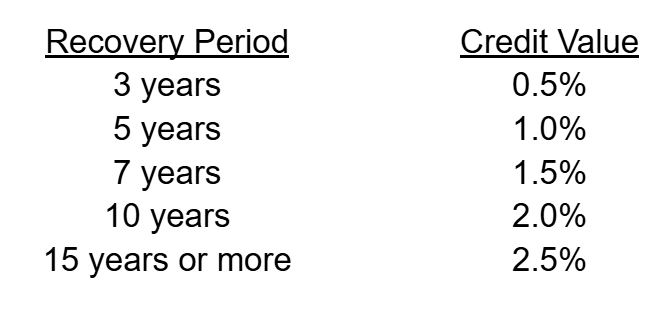

Investment Tax Credit: Manufacturers relocating to or expanding in South Carolina are eligible for a one-time corporate income tax credit based on the cost of new production equipment. The credit may offset up to 100% of corporate tax liability. Unused credits can be carried forward for up to 10 years from the year they are earned. This incentive applies specifically to investments in new production equipment.

Credit Values Based on Equipment Recovery Period:

Research and Development Tax Credit: South Carolina offers a tax credit equal to 5% of qualified research expenses incurred within the state. The credit cannot offset more than50% of a company’s remaining tax liability after applying other credits. Unused credits may be carried forward for up to 10 years.

Port Volume Increase Tax Credit: This program offers income tax credit or withholding tax credit for manufacturers, warehousers, distributors, freight forwarding companies, freight handling companies, and others who use a South Carolina port facility. A company must have 75 net tons of noncontainerized cargo, 385 cubic meters, or10 loaded TEUs transported in a base year and then increase that port cargo value by 5% year-over-year. Credit is limited to $15 million per year and unused credits may be carried forward for a period of 5 years.

Green Initiative Credits: South Carolina offers a variety of tax credits designed to encourage investments in green initiatives. Credits range from 25%-30% of qualified expenses and support activities such as recycling facilities, solar energy systems, energy conservation, renewable energy measures, and textile revitalization. Carryforward periods depend on the specific credit type, ranging from 5 years to indefinite.

Revitalization of Abandoned Building Credit: Companies may qualify for up to two credits for rehabilitating abandoned sites. Qualified sites must have at least 66% of their area nonoperational for at least five years before filing a Notice of Intent to Rehabilitate. One credit is against income or license taxes, equal to 25% of rehabilitation expenses, taken in equal installments over three years, starting the year the site is placed in service. This credit offsets up to 100% of tax liability, with an annual cap of $700,000 per tax year, and unused credits can be carried forward for five years. The second credit is against real property taxes, equal to 25% of rehabilitation expenses, offsetting up to 75% of property taxes for a maximum of eight years. The local county or municipality determines eligibility for the real property tax credit and must approve the project via public hearing and ordinance.

Fee-in-Lieu of Property Taxes (FILOT): Companies investing at least $2.5 million may negotiate with the county to reduce their property tax liability by lowering the assessment ratio from 10.5% to as low as6%, and stabilize millage rates for up to 30 years. Companies must meet the investment threshold within five years, with a potential five-year extension, allowing up to 10 years total to place eligible property under the fee. Real and personal property may qualify, but property previously on state tax rolls, including existing buildings, is not eligible unless an additional $45 million investment is made. Personal property under a FILOT depreciates, while real property is either fixed at its original cost or can be reappraised at fair market value by the South Carolina Department of Revenue every five years, depending on the agreement. Millage rates may be locked for the agreement’s duration or adjusted every five years. Additionally, a “Super Fee” is negotiable for projects investing at least $400 million or investing more than $150 million and creating at least 125 new jobs. This classification enables the fee to lower the assessment rate to as low as 4%.

Sales Tax Exemption: South Carolina offers extensive sales tax exemptions to support businesses. Exempt items include inventories, intangible personal property, research and development equipment, manufacturing equipment, industrial electricity, and fuels used in manufacturing. Construction materials used to build a manufacturing or distribution facility are exempt from sales tax if the company invests at least $100 million within an 18-month period. New or expanding technology-intensive companies may qualify for sales and use tax exemptions on computer equipment if they create at least 100 new jobs within five years, pay an average wage of at least 150% of the state per capita wage, and invest at least $300 million in real or personal property over five years, with 60% of the investment dedicated to computer equipment. For new or expanding recycling facilities investing at least $150 million by the fifth calendar year after beginning construction or operations, South Carolina provides exemptions on recycling equipment, electricity, and other specific property used in the facility.

Data Centers: Businesses that operate data centers may receive exemptions from sales and use taxes on materials including computer equipment, software, and electricity used directly in datacenter operations. To be eligible for the exemption, a data center must invest at least $50 million (or $75 million at a multi-tenant facility) and create at least 25 jobs with an average wage that is 150% of the county or state per capita wage, whichever is lower. The investment and jobs must be achieved over a five-year period, and the jobs must be maintained for an additional three years.

Property Tax Exemptions and Abatements: South Carolina exempts 14.8571% of the property tax value of manufacturing property assessed at the standard 10.5% ratio, with a statewide cap of $170 million annually. If the cap is exceeded, exemptions are proportionally reduced. This exemption was phased in over six years starting in2018 and excludes property under Fee-in-Lieu agreements. Additionally, a five-year abatement from county operating taxes is available for new or expanding manufacturing and R&D facilities investing at least $2,500,000, covering 25%-50% of local millage rates but excluding school district taxes. This abatement also excludes property under Fee-in-Lieu agreements to prevent overlapping benefits.

Corporate Income Tax Moratorium: Companies that create at least 100 new jobs within 5 years in certain economically distressed counties in South Carolina can qualify for a corporate income tax moratorium. Under this program, the Company’s entire state corporate income tax liability may be eliminated. At least 90% of the company’s total investment must be in a county where the unemployment rate is twice the state average. The length of the moratorium varies from 10 to 15 years and is contingent on the number of net new full-time jobs created. Chesterfield, Union, and Marlboro Counties are the only designated moratorium counties for 2026.

readySC and Apprenticeship Carolina: These two programs provide recruiting, training, and workforce development tools through the South Carolina Technical College System. Through the Apprenticeship program, eligible businesses can also receive a tax credit of up to $6,000 for each registered apprentice employed for at least 7 months during a year. ready SC™ provides services at no cost to eligible new or expanding companies. Additionally, South Carolina Commerce provides wage and demographic analysis at no cost to help businesses optimize recruitment and retention strategies. On-the-job training programs reimburse businesses up to and 75% of wages or salaries to offset the costs of training new employees, depending on company size and job requirements.

Last updated: April 2026

We're on a mission to help companies of all sizes identify the best locations, secure incentives, obtain development approvals and optimize energy strategies through Location Economics®.

BLS & Co. conducted a thorough review of Florida Power & Light’s 35-county territory to pre-qualify sites for data centers and other mission-critical facilities.

BLS & Co. and its energy services affiliate Sugarloaf Associates conducted a thorough review of Florida Power & Light’s 35-county territory to pre-qualify sites for data centers and mission-critical facilities. Four diverse sites were selected. The sites offer a unique combination of factors desired by today’s mission critical and data center operations, including highly reliable and redundant power and fiber infrastructures, competitive cost structures, and locations insulated from manmade and natural risks.

BLS/SLA also provided advisory service and expert witness in the development of a new FPL electric economic development rider for data centers and large manufacturing plants in Florida's FPL territory.

BLS & Co. utilizes an assortment of services – a process we call Location Economics® – to advise clients on location decisions. Discover our variety of offerings to help you navigate the complex decision making processes that occur when searching for a new location for your organization.

BLS & Co. specializes in a variety of industries and our dedicated team is compromised of experts in nearly all major categories.

At BLS & Co., we have executed wide variety of projects for our clients, which includes facilities such as headquarters, warehouses, and data centers.

Stay up to date with BLS & Co. by exploring our latest news and musings on the world of site selection and more.

We're proud to provide a few key resources to help get you started on your site selection journey.

Search our North American database for the right location for your company's HQ, R&D Facilities, and more.

Browse our regional resource guide for site selection in the U.S.

If your organization is confronting complex and sensitive location decisions, please reach out to schedule a confidential conversation.

Interested in a career opportunity with BLS & Co.? Click below to learn more about our growing team and view all current openings.