About

Services

Industries

Press & insights

resources

contact

We're on a mission to help companies of all sizes identify the best locations, secure incentives, obtain development approvals and optimize energy strategies through Location Economics®.

BLS & Co. conducted a thorough review of Florida Power & Light’s 35-county territory to pre-qualify sites for data centers and other mission-critical facilities.

BLS & Co. and its energy services affiliate Sugarloaf Associates conducted a thorough review of Florida Power & Light’s 35-county territory to pre-qualify sites for data centers and mission-critical facilities. Four diverse sites were selected. The sites offer a unique combination of factors desired by today’s mission critical and data center operations, including highly reliable and redundant power and fiber infrastructures, competitive cost structures, and locations insulated from manmade and natural risks.

BLS/SLA also provided advisory service and expert witness in the development of a new FPL electric economic development rider for data centers and large manufacturing plants in Florida's FPL territory.

BLS & Co. utilizes an assortment of services – a process we call Location Economics® – to advise clients on location decisions. Discover our variety of offerings to help you navigate the complex decision making processes that occur when searching for a new location for your organization.

BLS & Co. specializes in a variety of industries and our dedicated team is compromised of experts in nearly all major categories.

At BLS & Co., we have executed wide variety of projects for our clients, which includes facilities such as headquarters, warehouses, and data centers.

Stay up to date with BLS & Co. by exploring our latest news and musings on the world of site selection and more.

We're proud to provide a few key resources to help get you started on your site selection journey.

Search our North American database for the right location for your company's HQ, R&D Facilities, and more.

Browse our regional resource guide for site selection in the U.S.

If your organization is confronting complex and sensitive location decisions, please reach out to schedule a confidential conversation.

Interested in a career opportunity with BLS & Co.? Click below to learn more about our growing team and view all current openings.

Over the last five years, U.S. manufacturing has been pulled in two directions at once: buoyed by historic public and private investment yet constrained by structural shifts in technology, trade and talent. For business leaders weighing where to deploy capital, and for communities competing to attract it, the headline numbers on jobs and output no longer tell the full story.

The more important question is which kinds of manufacturing are growing, where they are choosing to locate, and why some facilities are adding workers while others are doing more with less. From a site selection perspective, these dynamics are redefining what makes a location competitive and what it will take to sustain manufacturing employment in the decade ahead.

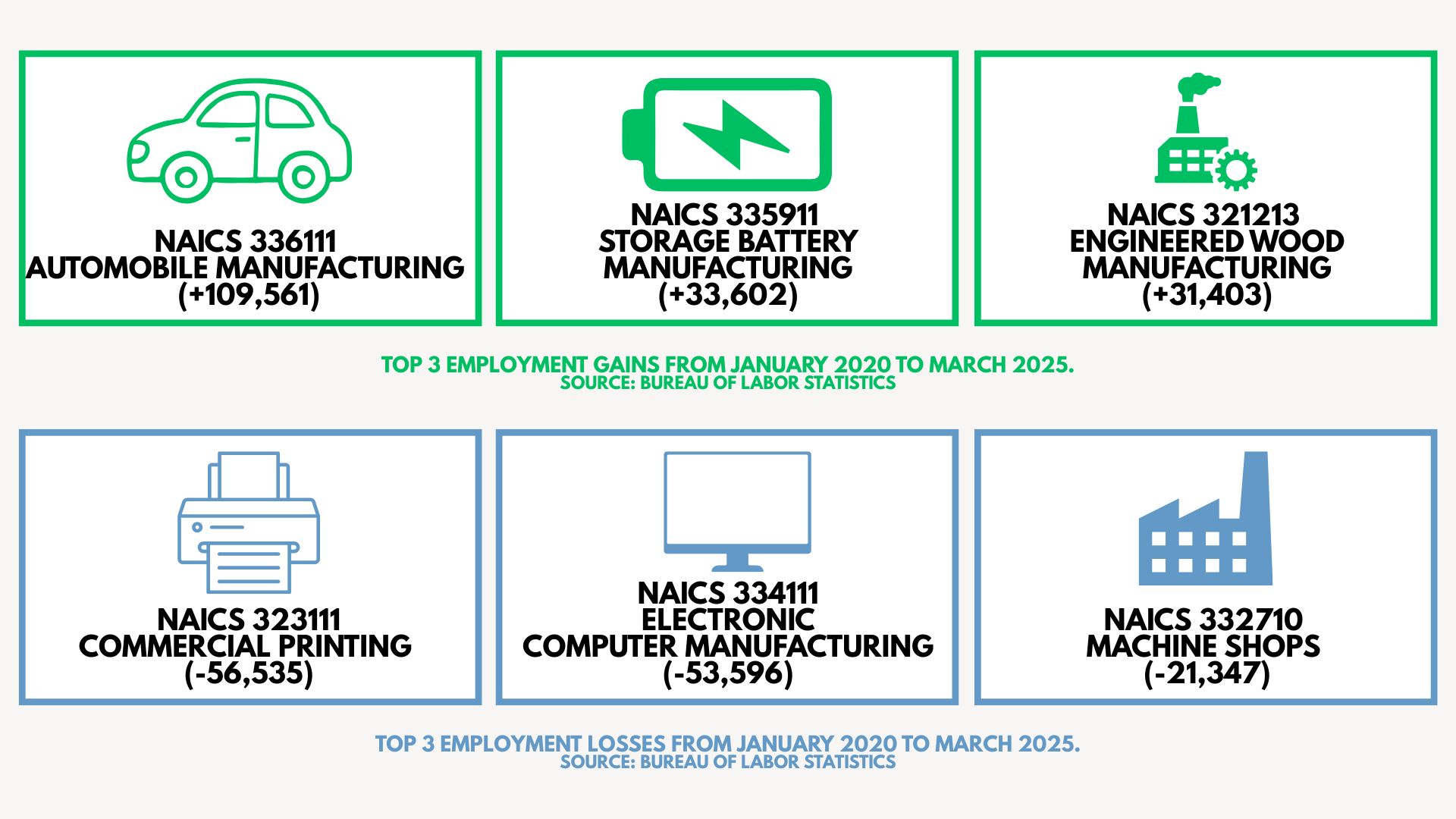

Between January 2020 and March 2025, the U.S. experienced a very slight increase in manufacturing employment, much of it attributed to a rebound from losses during the pandemic.

Industries tied to emerging technologies and domestic investment—including automobile manufacturing, storage battery production, and engineered wood—saw strong job gains. These gains were fueled by policy incentives, supply chain reshoring, growing demand, and the need for labor to support new production facilities, particularly for electric vehicles, battery systems, and sustainable construction materials.

Conversely, more traditional or mature manufacturing sectors—such as commercial printing, electronic computer manufacturing, and machine shops—faced employment declines. The primary drivers were structural shifts in demand, automation and productivity gains, offshoring of routine work, and workforce transitions, including retirements and fewer new entrants into skilled trades. Even as output in some of these sectors remained stable or grew, fewer workers were needed to meet production requirements.

Looking ahead, manufacturing employment may not rebound in the same way it has in prior cycles. Rapidly evolving trade policies, cost pressures, and continued automation will likely limit growth in traditional production roles. This does not signal a broad manufacturing contraction, but rather a continued redefinition of what manufacturing work looks like in today’s economy.

The next phase of growth will be driven less by high-volume labor and more by specialized, high-skill roles tied to advanced production, automation, materials science, data analytics, clean technology, and supply chain innovation.

Regions that invest in technical education, reskilling programs, apprenticeships, and strong partnerships between industry and higher education will be best positioned to capture this new wave of manufacturing investment.

Tracey Hyatt Bosman develops and executes incentives and location selection strategies for BLS & Co.'s corporate and institutional clients. She is a certified economic developer with twenty years of professional experience across a wide range of sectors, including data centers, manufacturing, headquarters, back office and contact center operations, and logistics.

We're on a mission to help companies of all sizes identify the best locations, secure incentives, obtain development approvals and optimize energy strategies through Location Economics®.

BLS & Co. conducted a thorough review of Florida Power & Light’s 35-county territory to pre-qualify sites for data centers and other mission-critical facilities.

BLS & Co. and its energy services affiliate Sugarloaf Associates conducted a thorough review of Florida Power & Light’s 35-county territory to pre-qualify sites for data centers and mission-critical facilities. Four diverse sites were selected. The sites offer a unique combination of factors desired by today’s mission critical and data center operations, including highly reliable and redundant power and fiber infrastructures, competitive cost structures, and locations insulated from manmade and natural risks.

BLS/SLA also provided advisory service and expert witness in the development of a new FPL electric economic development rider for data centers and large manufacturing plants in Florida's FPL territory.

BLS & Co. utilizes an assortment of services – a process we call Location Economics® – to advise clients on location decisions. Discover our variety of offerings to help you navigate the complex decision making processes that occur when searching for a new location for your organization.

BLS & Co. specializes in a variety of industries and our dedicated team is compromised of experts in nearly all major categories.

At BLS & Co., we have executed wide variety of projects for our clients, which includes facilities such as headquarters, warehouses, and data centers.

Stay up to date with BLS & Co. by exploring our latest news and musings on the world of site selection and more.

We're proud to provide a few key resources to help get you started on your site selection journey.

Search our North American database for the right location for your company's HQ, R&D Facilities, and more.

Browse our regional resource guide for site selection in the U.S.

If your organization is confronting complex and sensitive location decisions, please reach out to schedule a confidential conversation.

Interested in a career opportunity with BLS & Co.? Click below to learn more about our growing team and view all current openings.