About

Services

Industries

Press & insights

resources

contact

BLS & Co. periodically revises the state incentive pages to ensure our firm is providing the most current information on legislative and regulatory developments affecting available programs. Updates will be posted in the near future. In the interim, please call BLS & Co. with any questions at 609.924.9775 or reach out via email at info@BLSstrategies.com.

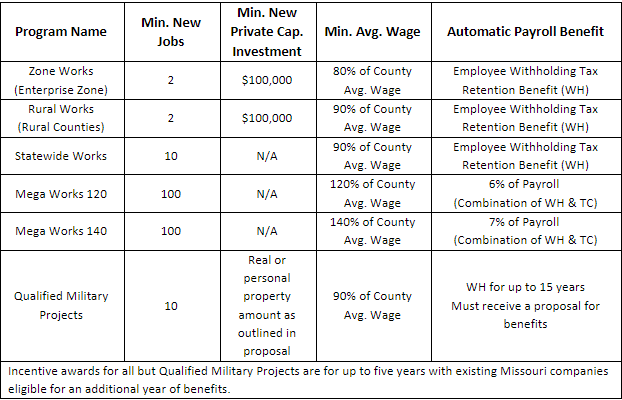

Missouri Works: Businesses that create new full-time jobs in Missouri may be eligible for a tax incentive and payroll benefit through the Missouri Works program which awards businesses the ability to retain the state withholding taxes of newly created jobs and, in some cases, receive a refundable, sellable, or transferable corporate income tax credit equivalent to a percentage of new payroll created.

Incentive awards for all but Qualified Military Projects are for up to five years with existing Missouri companies eligible for an additional year of benefits. The actual value of the incentive award will be based on the number of jobs created, project location, and total payroll. The minimum average wage requirement for the program is the lesser of the county average wage or the statewide average wage.

For high-impact projects, the state can award an additional payroll benefit award beyond the automatic benefit listed as additional tax credits. In addition, the state can award a highly discretionary “deal closing fund” award whereby the full value of the total tax credit award over the life of the award can be claimed in the first year to accelerate benefits and offset project upfront costs.

Business Use Incentives for Large Scale Development (BUILD) Bonds: Large economic development projects locating in Missouri may be eligible for refundable tax credits generated through the BUILD financing program. Through the program, a project’s capital investment in infrastructure is financed through BUILD bonds with the company making principal and interest payments. The Department of Revenue issues refundable tax credits equal to the debt service payments for the company to use effectively making the program a grant reimbursement for the infrastructure costs incurred. To be eligible, manufacturing and R&D projects must invest a minimum of $15 million and create at least 100 jobs. Office and headquarters projects must invest a minimum of $10 million and create at least 500 jobs (200 if in a distressed community).

Business Facility Headquarters Tax Credit Program: This program provides tax incentives to facilitate the expansion of new or existing business in Missouri. Eligible business facilities include engineering firms, architectural firms, and accounting firms. To receive tax credits in any of the ten years the facility must create 25 new jobs and make $1 million in investment in that year compared to the base year. They also must maintain a total new facility investment of at least $20 million and total employment of at least 500 new facility employees.

R&D Tax Credit: State income tax credit equivalent to 15% of qualified research expenses. Companies can receive an additional 5% credit for qualifying research expenses related to research conducted with a Missouri-based university. The program has a credit cap of $10 million annually with no single company allowed to receive more than $300,000 in credits per year. Of the $10 million cap, $5 million is reserved for minority and women business enterprises and small businesses. New businesses, defined as a business less than five years old, are issued full tax credits first.

Data Center Sales and Utility Tax Exemption: Businesses that create 10 full-time jobs with wages that are at or above 150% of the county average wage and invest $25 million in a new data center facility within a 36-month window may receive a full 15-year exemption of sales and utility taxes associated with the data center. A 10-year exemption is available for companies that expand an existing data center facility by investing $5 million within 12 months and creating at least 5 full-time jobs with wages that are at or above 150% of the county average wage within 24 months. In addition, a consortium of eligible companies may aggregate their jobs and investment at the same facility to achieve the minimum thresholds.

Sales Tax Exemption for Manufacturers and R&D: Electrical energy, gas, water, coal, energy sources, chemicals, machinery equipment, and materials used or consumed in a manufacturing or R&D process is exempt from sales and use tax.

Missouri One Start: Missouri’s training programs are designed to be flexible so companies can effectively recruit and train their current and future workforce in new or improved processes. Funding can be targeted to include areas such as technical training, quality training, or soft skills training. Eligible companies can be reimbursed for training expenses incurred through hired training partners, community colleges, their own internal resources, or any combination of all three. Training awards typically average $1,000-$3,000 per qualified employee, and the overall level of assistance is determined by the number of jobs, the wages, and availability of resources.

Advanced Industrial Manufacturing Zones Act: This act establishes the Port Authority AIM Fund which consists of 50% of the state withholding tax from new jobs within the zone after the development or redevelopment has begun. The zones are identified and established through resolution by Port Authority commissioners. To be eligible for the retention tax withholdings there must be an increase in the number of full-time employees located at the facility. New employees must be paid at or above the state average wage. The AIM Zone Fund may be used for managerial, engineering, legal, research, promotion, planning, satisfaction of bonds, and any other expenses.

Chapter 100 Industrial Revenue Bonds: Local governments in Missouri can offer real and/or personal property tax abatements to businesses through the issuing of Chapter 100 Industrial Revenue Bonds. Companies eligible for Chapter 100 bond financing include manufacturing, warehousing, distribution, office, research and development, agricultural processing, and services in interstate commerce. In the St. Louis and Kansas City metropolitan areas, local governments can provide similar tax abatements and exemptions through their corresponding Land Clearance for Redevelopment Authorities or their Port Authorities.

The incentive can also provide a sales tax exemption on tangible personal property purchased through Chapter 100 bonds for non-manufacturing purchases as well as building materials for real property investment.

Last Updated: April 2023

We're on a mission to help companies of all sizes identify the best locations, secure incentives, obtain development approvals and optimize energy strategies through Location Economics®.

BLS & Co. conducted a thorough review of Florida Power & Light’s 35-county territory to pre-qualify sites for data centers and other mission-critical facilities.

BLS & Co. and its energy services affiliate Sugarloaf Associates conducted a thorough review of Florida Power & Light’s 35-county territory to pre-qualify sites for data centers and mission-critical facilities. Four diverse sites were selected. The sites offer a unique combination of factors desired by today’s mission critical and data center operations, including highly reliable and redundant power and fiber infrastructures, competitive cost structures, and locations insulated from manmade and natural risks.

BLS/SLA also provided advisory service and expert witness in the development of a new FPL electric economic development rider for data centers and large manufacturing plants in Florida's FPL territory.

BLS & Co. utilizes an assortment of services – a process we call Location Economics® – to advise clients on location decisions. Discover our variety of offerings to help you navigate the complex decision making processes that occur when searching for a new location for your organization.

BLS & Co. specializes in a variety of industries and our dedicated team is compromised of experts in nearly all major categories.

At BLS & Co., we have executed wide variety of projects for our clients, which includes facilities such as headquarters, warehouses, and data centers.

Stay up to date with BLS & Co. by exploring our latest news and musings on the world of site selection and more.

We're proud to provide a few key resources to help get you started on your site selection journey.

Search our North American database for the right location for your company's HQ, R&D Facilities, and more.

Browse our regional resource guide for site selection in the U.S.

If your organization is confronting complex and sensitive location decisions, please reach out to schedule a confidential conversation.

Interested in a career opportunity with BLS & Co.? Click below to learn more about our growing team and view all current openings.